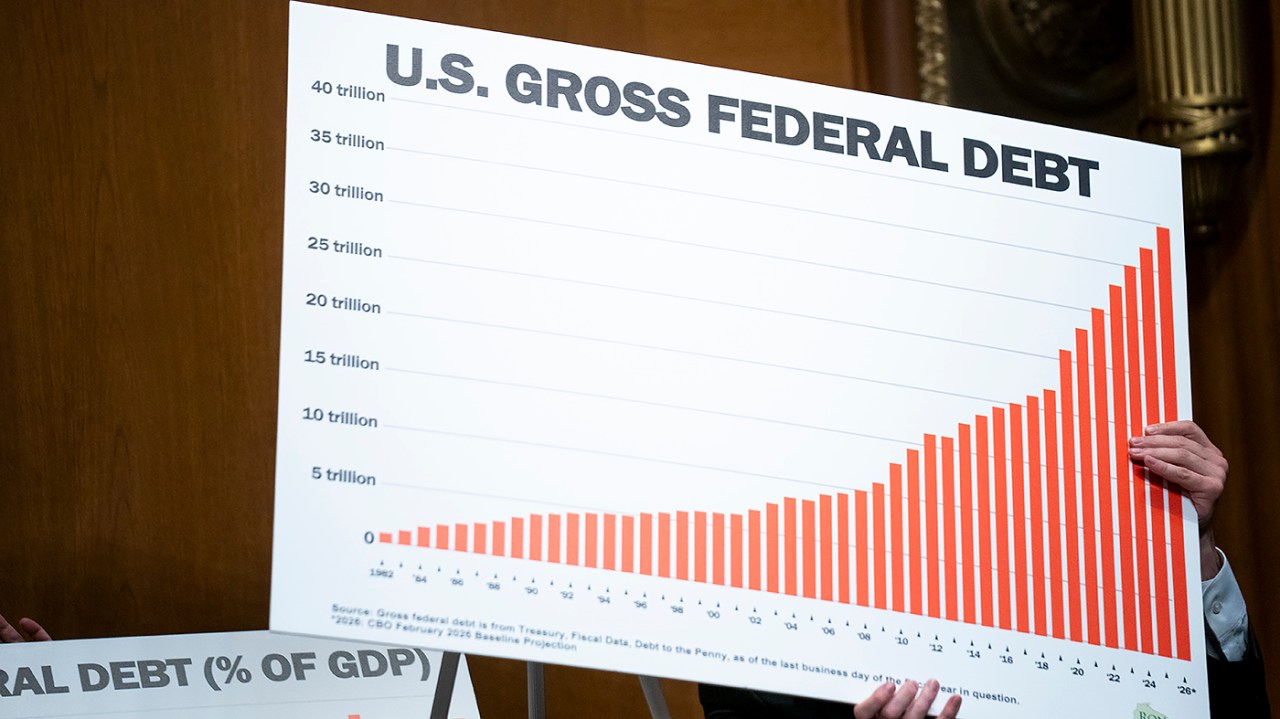

The U.S. national debt has now surpassed the gross domestic product (GDP), reaching 100.2 percent of GDP at the end of March. This signifies a significant shift, with debt held by the public totaling $31.27 trillion against a GDP of $31.22 trillion over the past year. Experts warn this is uncharted territory, indicating that borrowing has occurred not due to global conflict, but a “bipartisan abdication of making hard choices.” Projections suggest that if current fiscal policies remain unchanged, the debt held by the public could rise to 108 percent of GDP by 2030, underscoring the unsustainable fiscal trajectory.

Read the original article here

The United States debt has now surpassed the total value of its economy, meaning our national debt is more than 100% of our Gross Domestic Product (GDP). This is a significant economic milestone, and it’s understandable why it’s a topic of such intense discussion and concern. It signifies a point where the nation owes more than it produces in a given year, a situation that can have far-reaching implications for our financial future and the well-being of generations to come.

The reality of this debt level is a complex issue, and it’s particularly striking when we consider the historical context and the often-divergent viewpoints surrounding fiscal responsibility. For years, there’s been a vocal emphasis on the dangers of national debt, especially when certain political parties are in power. We’ve seen and heard cries about deficits, balanced budgets, and the perils of “tax and spend” policies, often directed at Democratic administrations.

However, this current situation, where the debt has ballooned past GDP, highlights a stark inconsistency for some. The very individuals and groups who have historically been the loudest critics of rising debt seem to have a remarkably different perspective when their own party is in control. The narrative often shifts, and concerns about the deficit appear to fade, leading to accusations of hypocrisy.

It’s often observed that when Republicans are in power, there’s a tendency to implement policies that increase the national debt, such as significant tax cuts, particularly for corporations and the wealthy. These cuts, while potentially stimulating certain sectors of the economy in the short term, do not always translate into proportional revenue increases for the government. Instead, they can widen the gap between government spending and income, directly contributing to a growing national debt.

This pattern of behavior, where fiscal conservatism seems to be selectively applied, is a significant point of contention. The argument is that the debt only truly “matters” and becomes a national crisis when a Democrat is in the White House. When Republicans are in charge, however, these concerns are often sidelined, and the focus shifts to other priorities, sometimes leading to accusations that public funds are being diverted for the benefit of specific groups or individuals.

One of the most concerning potential consequences of such a high debt-to-GDP ratio is the specter of inflation. When a government consistently spends more than it earns, and particularly if it resorts to printing more money to cover its obligations, it can devalue the currency. This erosion of purchasing power is precisely what inflation is, and it can disproportionately affect ordinary citizens, making everyday goods and services more expensive and diminishing the value of savings.

This leads to a broader point about how many Americans perceive their own financial situation. There’s a perceived disconnect between the economic realities and the self-image of prosperity that many hold. In a global context, it’s often noted that while many Americans might be living paycheck to paycheck or facing precarious financial situations, there’s a prevailing sense of national wealth and individual affluence that doesn’t necessarily reflect the underlying economic vulnerabilities. This “imagined wealth” can make it harder to acknowledge and address the serious consequences of a ballooning national debt.

The idea that economic prosperity is simply a matter of printing more money or relying on superficial indicators like a rising stock market, while ignoring the fundamental issues of debt and revenue, is a dangerous oversimplification. The stock market can be influenced by many factors and doesn’t always reflect the true economic health of the nation or the financial well-being of its citizens. True prosperity comes from sustainable economic growth, responsible fiscal management, and policies that benefit the broad populace, not just a select few.

This situation also raises questions about the long-term sustainability of our economic model. If the U.S. continues on this trajectory, with debt exceeding its economic output, it can lead to a loss of confidence from international partners and investors. At some point, the “house of cards,” as some might describe it, could become unstable, and those who have lent money might become less willing to do so, or demand significantly higher interest rates, further exacerbating the debt problem.

The notion of “winning,” often used in political rhetoric, becomes particularly ironic in this context. If “winning” means accumulating record levels of debt and potentially jeopardizing the nation’s economic stability, then it’s a hollow victory. The idea that leaders are solely focused on short-term political gains or catering to specific interest groups, without regard for the long-term consequences for future generations, is a source of deep concern.

It’s important to acknowledge that addressing a national debt of this magnitude is not a simple task. It often requires difficult choices and unpopular decisions. However, the current path, characterized by a disregard for fiscal discipline when it’s politically inconvenient and a continued reliance on unsustainable spending, feels like a point of no return for some observers.

Ultimately, when the national debt surpasses 100% of GDP, it’s more than just a number; it’s a warning sign. It signals a potential erosion of our own prosperity and that of those who will inherit the nation’s economic burdens. The question remains whether the political will exists to confront this challenge honestly and effectively, or if the cycle of fiscal irresponsibility will continue, with dire consequences for the future.