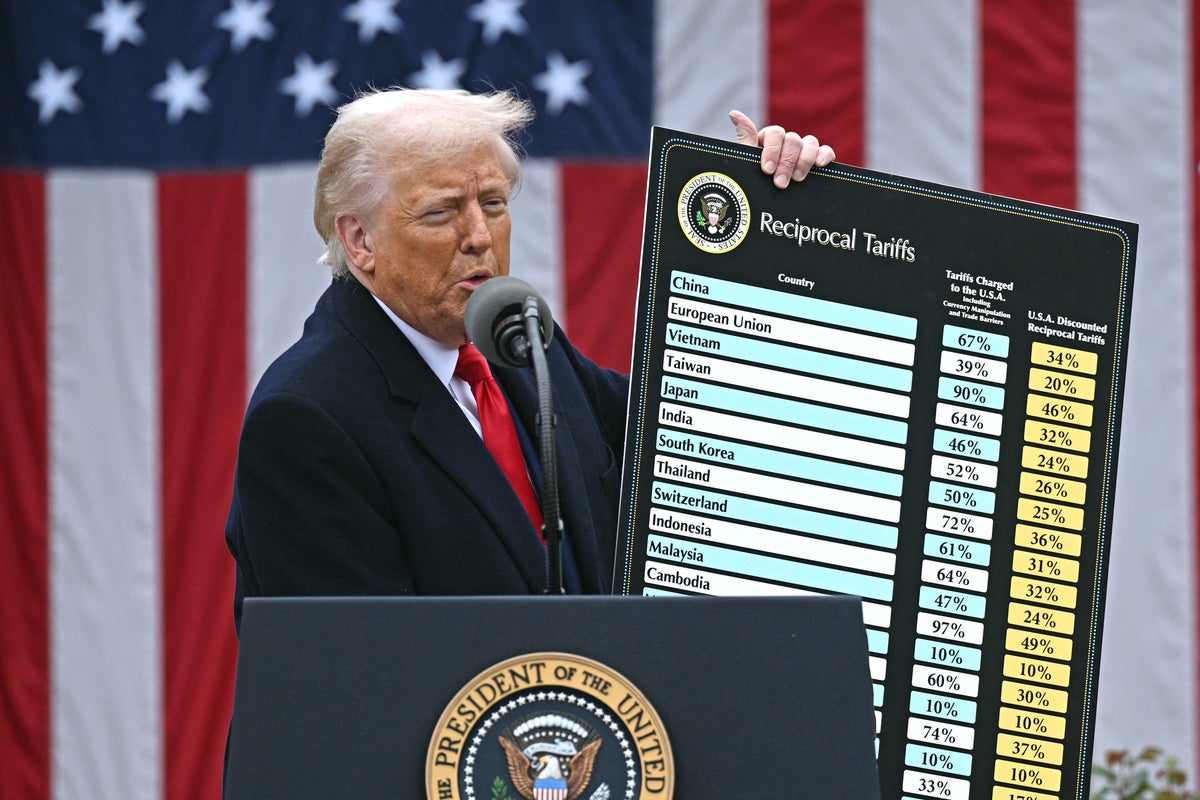

President Trump made 327 stock purchases of major tech companies shortly before announcing a pause on his tariffs, a move that caused stock prices, including those he invested in, to surge. This timing has drawn accusations of corruption and self-enrichment from Democrats, who cite significant financial gains made during his presidency. While White House spokespeople deny any conflict of interest, asserting his assets are managed independently, the unprecedented windfalls have raised concerns among experts and political figures.

Read the original article here

Recent financial disclosures have brought to light a fascinating, and for some, alarming, pattern of activity: 327 stock purchases made by Donald Trump just days before a significant market shift, attributed by some to a pause in his tariff policies. These disclosed transactions, reportedly occurring on April 8, 2025, place the purchases a mere six days after the initiation of a global trade war and, strikingly, the day before a prominent post on his social media platform declaring, “THIS IS A GREAT TIME TO BUY!!!”

The timing of these extensive stock buys, coinciding so closely with major policy pronouncements that could directly influence market behavior, has ignited conversations about the intersection of presidential power and personal financial gain. It’s a scenario that prompts questions about the team managing these transactions and whether they operate with an awareness of impending presidential actions that could impact stock values. The sheer volume of purchases, 327 in total, suggests a deliberate and extensive strategy rather than a casual investment.

Many observers view these disclosures as further evidence of a system where financial gain is interwoven with political decisions. The argument is made that Trump’s actions, from trade wars to other policy shifts, are not solely for the benefit of the nation but are often linked to personal profit. This perspective suggests that elements of his administration’s agenda, whether it’s slashing federal programs or imposing tariffs, may be designed to create market conditions that are advantageous for his own holdings.

The notion of “pure stock market manipulation” arises when considering these events. The idea is that by strategically implementing or pausing trade policies, a president could create predictable market fluctuations. The subsequent declaration of it being a “great time to buy” then acts as a potential signal, leading to a market surge that benefits those who invested beforehand, including, as the disclosures suggest, the president himself. This alleged cycle of policy, market impact, and personal enrichment is a central concern being raised.

Furthermore, the contrast between Trump’s approach to personal investments and that of previous presidents is often highlighted. The tradition of placing personal assets into a blind trust is meant to preempt any appearance of impropriety or conflicts of interest. The fact that Trump has not followed this established norm, according to many, amplifies concerns about the potential for self-dealing and profiting from the office. This lack of a blind trust is seen by some as a direct indicator of a willingness to engage in actions that could benefit his personal wealth.

The sentiment that “America is done” or that the country is heading towards a dictatorship is often expressed in light of these financial disclosures and the perceived lack of consequences. The concern is that if such actions are not met with serious repercussions, it sets a dangerous precedent. The observation that the GOP Congress appears to be largely silent on these matters, “whistling in the breeze,” contributes to the feeling that checks and balances are failing, allowing for what some describe as “absolute corruption.”

The comparison to Martha Stewart’s legal troubles is frequently brought up to underscore the perceived double standard. The argument is that if an individual outside of the highest office can face severe penalties for insider trading or similar financial improprieties, then a president engaged in what many perceive as even more egregious acts should face equally, if not more, stringent consequences. The sheer scale of the alleged actions by Trump, in this view, dwarfs past cases, yet the expectation of accountability appears diminished.

The public pronouncements about immense stock market gains during his term, coupled with these disclosures, lead many to believe that this is not a matter of luck or astute business acumen but rather a calculated manipulation of his presidential power. The descriptor “Commander in Thief” reflects this deep-seated belief that his presidency has been characterized by corruption for personal and political gain. The lack of significant public outcry or official action, in this context, is seen as evidence of a systemic breakdown.

The possibility that not just Trump himself, but also his family and associates, may have benefited from this alleged insider knowledge is another recurring theme. The “most corrupt administration in US history” is a label used to encapsulate the perception that a culture of graft and personal enrichment has permeated his time in office. The current power dynamic, where many in positions of authority are beholden to him, is seen as a major obstacle to accountability, with the hope that a shift in power will bring about a change in tune and enable justice.

The urgency to pass certain legislation, such as the “save America act,” is interpreted by some as a move to consolidate power and avoid future accountability, suggesting a desire for “corruption without interruption.” The calls for indictment, prosecution, and imprisonment reflect a strong desire for legal and ethical standards to be upheld, irrespective of one’s position. The idea that no one is above the law is a core tenet being invoked in these discussions.

The potential for Trump’s actions to influence global economic trends, such as de-dollarization, is also considered. While some might debate whether his motives are purely for personal greed or a broader geopolitical strategy, the focus for many remains on the immediate impact of his policies on the stock market and his personal wealth. The narrative is that he is aggressively pursuing every opportunity for financial gain, and those who supported him are seen as having fallen for a “scam.”

The observation that certain conservative subreddits might be less inclined to discuss these financial disclosures, while readily highlighting similar accusations against Democrats, is often pointed out as a partisan double standard. The prevailing view expressed is that a stricter ethical code should apply to all public officials, regardless of political affiliation. The question of whether this constitutes “straight up insider trading” and why such actions are not being investigated with more vigor is a central point of contention.

The question of what mechanisms are in place to prevent such perceived corruption at the executive level, and why they appear to be failing, is a profound one. The current political climate, where loyalty to a particular leader can override institutional checks and balances, is seen as a significant factor. The hope is that through future elections, and potentially through legal means, accountability will eventually be achieved, and justice will be served for actions deemed unlawful and corrupt.