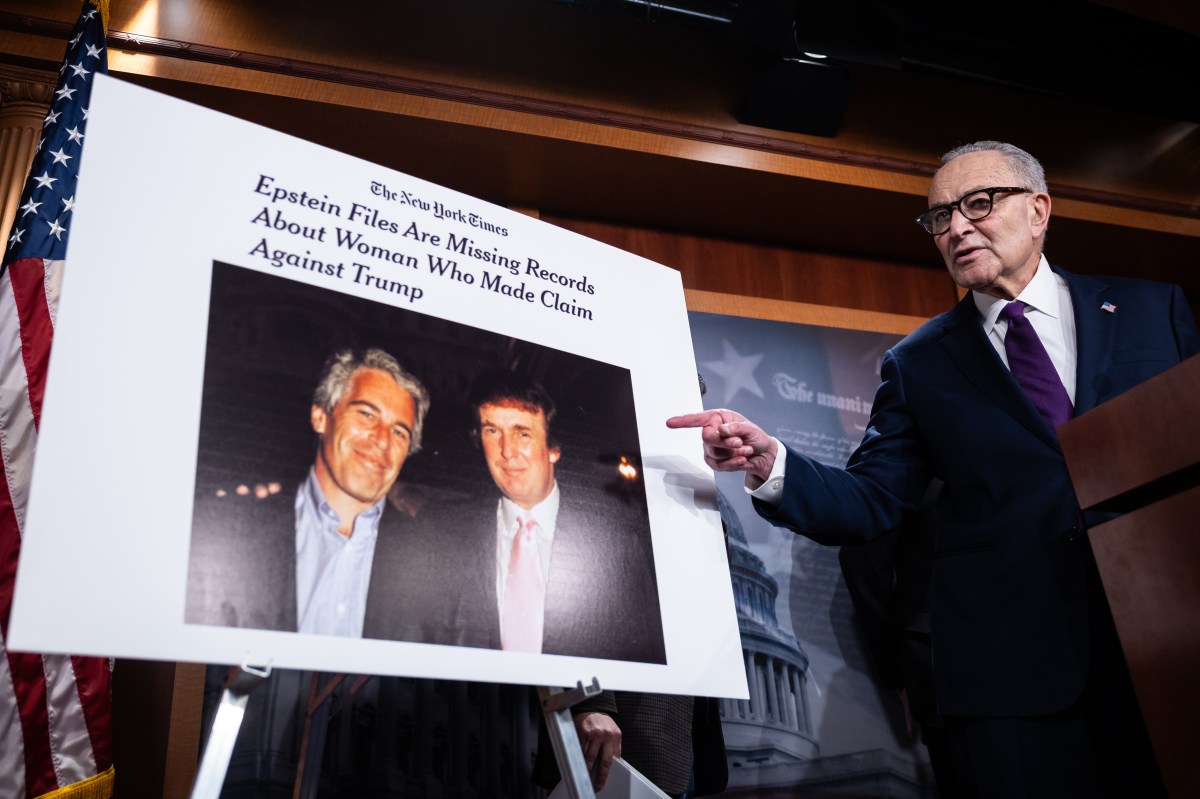

During a deposition, Jeffrey Epstein’s longtime accountant and estate co-executor Richard Kahn reportedly told House investigators that the estate settled with an accuser who had also made allegations concerning President Donald Trump. This account, relayed by a Democratic lawmaker, was juxtaposed with statements from the committee chair who stated Kahn saw no transactions to Trump or his family. Kahn’s prepared remarks maintained his ignorance of Epstein’s abuse until after his death, asserting he would have resigned had he known. The estate has already paid over $100 million to survivors, underscoring the ongoing liabilities and the focus of Congress on Epstein’s network and finances.

Read the original article here

A recent development suggests that the estate of Jeffrey Epstein may have provided a settlement payment to an accuser who had also brought allegations against Donald Trump. This information surfaced through testimony from an accountant involved in the estate’s financial dealings. The accountant, speaking to CBS News after a closed-door interview, detailed this payment related to an accuser who had leveled accusations against both Epstein and Trump.

The implications of this revelation are significant, especially considering the existing public discourse surrounding both Epstein and Trump. It paints a picture of financial entanglements that could further complicate already complex legal and ethical landscapes. The fact that the Epstein estate, rather than any individual directly, is reportedly the source of this settlement payment to an accuser who also targeted Trump is a point of considerable interest.

Adding a layer of complexity, reports indicate differing accounts regarding the specifics of these financial transactions. Representative James Comer, the Republican chair of the House Oversight Committee, reportedly stated that the accountant had “never seen any type of transaction to Trump or anyone in his family.” This statement appears to contrast with the narrative that an accuser related to Trump’s alleged misdeeds received a payoff. The presence of these differing accounts naturally raises questions about accuracy and potential motivations behind the statements.

The core of the discussion revolves around whether these payments were directly to Trump, to his family, or to individuals associated with him in a capacity that sought to resolve allegations. The distinction between “to Trump” and “from Trump” or “for Trump” becomes crucial in understanding the flow of money and the potential involvement of the former President. The accountant’s statement, as relayed, suggests a lack of direct transactions *to* Trump or his family, which Comer seemingly emphasized.

However, the broader context implies that even if not a direct financial transfer to Trump himself, the settlement payout to an accuser with claims against him could still be interpreted as an indirect resolution of issues tied to his alleged conduct. The idea that someone associated with Epstein’s network would facilitate a payment to settle claims involving a high-profile figure like Trump suggests a coordinated effort to manage fallout and avoid further scandal.

The mention of multiple clients paying money to Epstein by Comer, while downplaying direct transactions to Trump, could be seen as an attempt to narrow the scope of the investigation. The argument that this is a payoff to an accuser/victim, and not necessarily a direct transaction *from* Trump, is being made, but the fact of a settlement itself can be a powerful indicator.

The discussion around these settlements often circles back to the broader allegations against Trump, including past accusations of sexual misconduct. For those who believe these allegations are credible, this settlement payment from the Epstein estate to an accuser who also targeted Trump is not surprising. It aligns with a perception that wealth and influence can be used to manage or suppress accusations, irrespective of their veracity.

The timing of these revelations, and the ongoing scrutiny of Epstein’s network and its connections, suggests that more information could continue to emerge. The concept of “following the money” is frequently invoked in such investigations, as financial trails can often lead to unexpected places and reveal hidden relationships or activities. The current situation appears to be a prime example of this principle in action.

The question of who is being truthful in these differing accounts—Comer or the accountant relaying the information—is central to dissecting the event. Past political affiliations and observed behaviors are being used by some to infer potential biases. For those already skeptical of Trump’s involvement in scandals, any indication of financial settlements related to such accusations, regardless of the direct source, strengthens their existing convictions.

Ultimately, the report of the Epstein estate paying a settlement to an accuser who also targeted Donald Trump introduces a new, albeit potentially indirect, financial link into the ongoing discussions surrounding both figures. The full scope and impact of this settlement, and the accuracy of the various interpretations, will likely continue to be debated and investigated. The desire for transparency and the release of further documentation is a recurring theme, as many believe it is essential to fully understand the extent of these complex entanglements.