The Trump administration’s resumption of student loan collections has resulted in the garnishment of Social Security benefits for over 450,000 defaulted borrowers aged 62 and older, beginning as early as June. While up to 15% of benefits may be offset, leaving a minimum of $750, borrowers can challenge garnishments by proving financial hardship or pursuing loan discharge options, such as a Total and Permanent Disability discharge. Alternative solutions include getting current on loans through income-driven repayment plans or utilizing available resources to supplement income. The 15% cap applies to all Social Security benefits, including retirement and disability payments.

Read the original article here

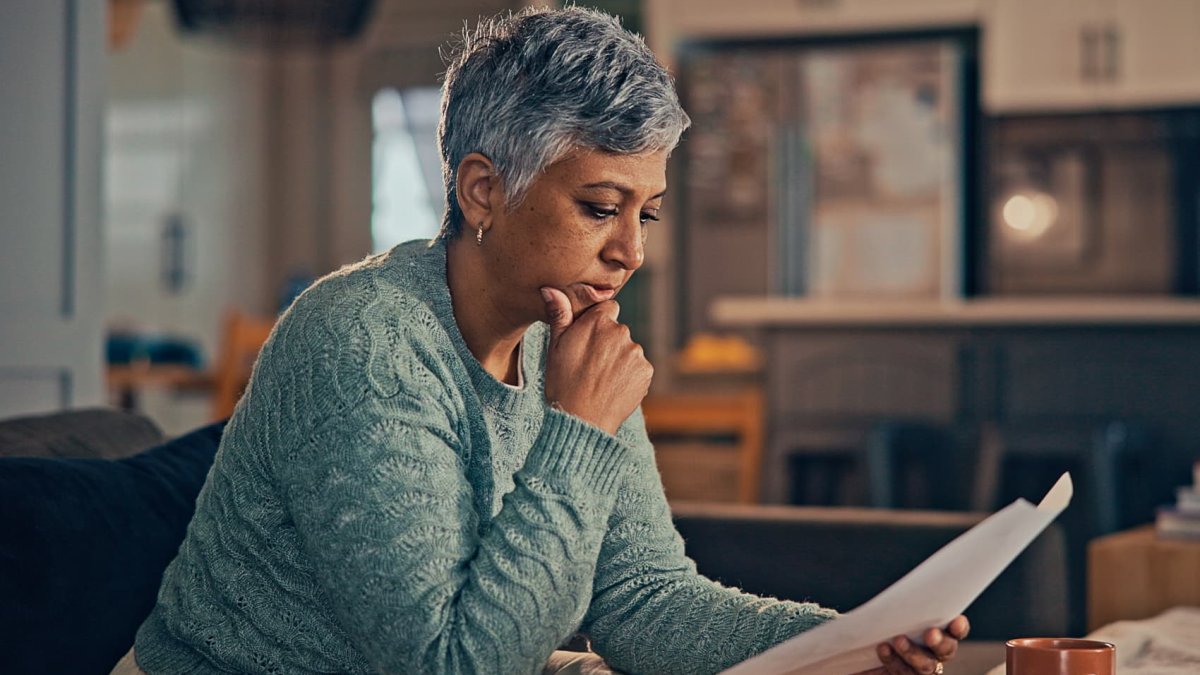

Social Security checks may be smaller starting in June for some recipients, as the resumption of student loan garnishments gets underway. This means that for some retirees and those receiving disability benefits, a portion of their monthly payments will be redirected towards outstanding student loan debt. This development is sparking considerable concern and debate, especially given the potential financial hardships it could create for vulnerable individuals.

The situation highlights a critical intersection between retirement security and the burden of student loan debt. Many individuals are facing the stark reality of having their retirement funds, intended to support them in their later years, diminished to cover loans they may have taken out decades ago. For some, this could mean the difference between maintaining their current living standard and facing significant financial distress.

One of the key frustrations voiced is the seeming permanence of student loan debt. Unlike other forms of debt, student loans often cannot be discharged through bankruptcy, leaving many feeling trapped in a cycle of repayment that stretches far beyond their working years. This is especially true for individuals who have diligently made payments for years, only to find that the interest accumulated has increased their overall loan balance significantly. The sentiment expressed is one of unfairness, considering the high cost of education and the fact that many borrowers have paid back far more than their initial principal amount.

The impact of this policy is expected to disproportionately affect vulnerable populations. Many individuals facing garnishment are disabled, orphaned, or have assumed their children’s student loan debt. The fact that these individuals, already facing financial challenges, are now seeing their retirement security jeopardized raises ethical concerns. The system, intended to provide a safety net, is instead contributing to their financial vulnerability.

The issue of student loan forgiveness has been central to the discussion surrounding this policy. The belief that the government should step in to alleviate the burden of this debt has found many proponents, but there is also a counter argument. Even those opposed to broad-based forgiveness often advocate for reforms that address issues such as excessive interest rates and the inability to discharge loans through bankruptcy. The sentiment is that the current system is broken, leaving many borrowers with insurmountable debt and impacting their economic well-being far beyond graduation.

Several suggestions for reform have emerged, including capping interest rates, potentially at a rate that accounts for inflation, and allowing for loan forgiveness after a certain number of payments have been made that equal or exceed the initial principal. Others advocate for revisiting the eligibility criteria for student loans and implementing more stringent lending practices. The desire for more responsible lending practices, which protect both borrowers and lenders, is apparent.

A key factor contributing to the crisis is the lack of risk for banks issuing student loans. The inability to default on these loans removes any financial incentive for banks to engage in responsible lending, leading to the issuance of loans to individuals without a realistic expectation of repayment. This creates a vicious cycle that perpetuates the student loan crisis. The system, as it stands, does little to address these underlying issues.

The political ramifications of the policy are also being debated. The perception that those who chose to vote for certain political parties are now experiencing the consequences of those choices has fueled considerable animosity, alongside criticism that specific campaigning strategies ignored the economic concerns of many voters. This demonstrates the complex interplay between political considerations and financial policy. The frustration extends to the broader political discourse around student loan debt, highlighting the challenges of finding bipartisan solutions to complex economic problems.

In conclusion, the resumption of student loan garnishments for Social Security benefits presents a significant financial challenge for many recipients. The intersection of student loan debt and retirement security is a complex and contentious issue that requires comprehensive reform. Addressing the lack of risk for lenders, establishing fairer interest rates, and providing opportunities for loan forgiveness are steps that could mitigate the negative impacts of this policy on vulnerable populations, and alleviate the anxieties of countless retirees and individuals receiving disability benefits.